Table of Contents

[ad_1]

I toured a $9 million house in Honolulu to better understand the luxury housing market. I love real estate, and visiting nice homes for sale is one of my favorite hobbies.

My parents are 81 and 78 and live in Honolulu. Like many people their age, they have a few health issues, and I’d like to be there to help take care of them.

Since we’re flexible and can live anywhere, my wife and I plan to relocate to Honolulu in 2029, once the school entry timing works for our kids. There, we’ll take my parents to doctor appointments, fix things around their house, get them food, and simply spend more time together while we can.

A home purchase that far out is one of the biggest financial decisions we’ll ever make, so I’m doing what I always tell you to do. I’m studying the market years in advance. Touring open houses is free education. The more homes you see, the better calibrated you become on value, and the less likely you are to make an emotional mistake when it’s finally time to buy.

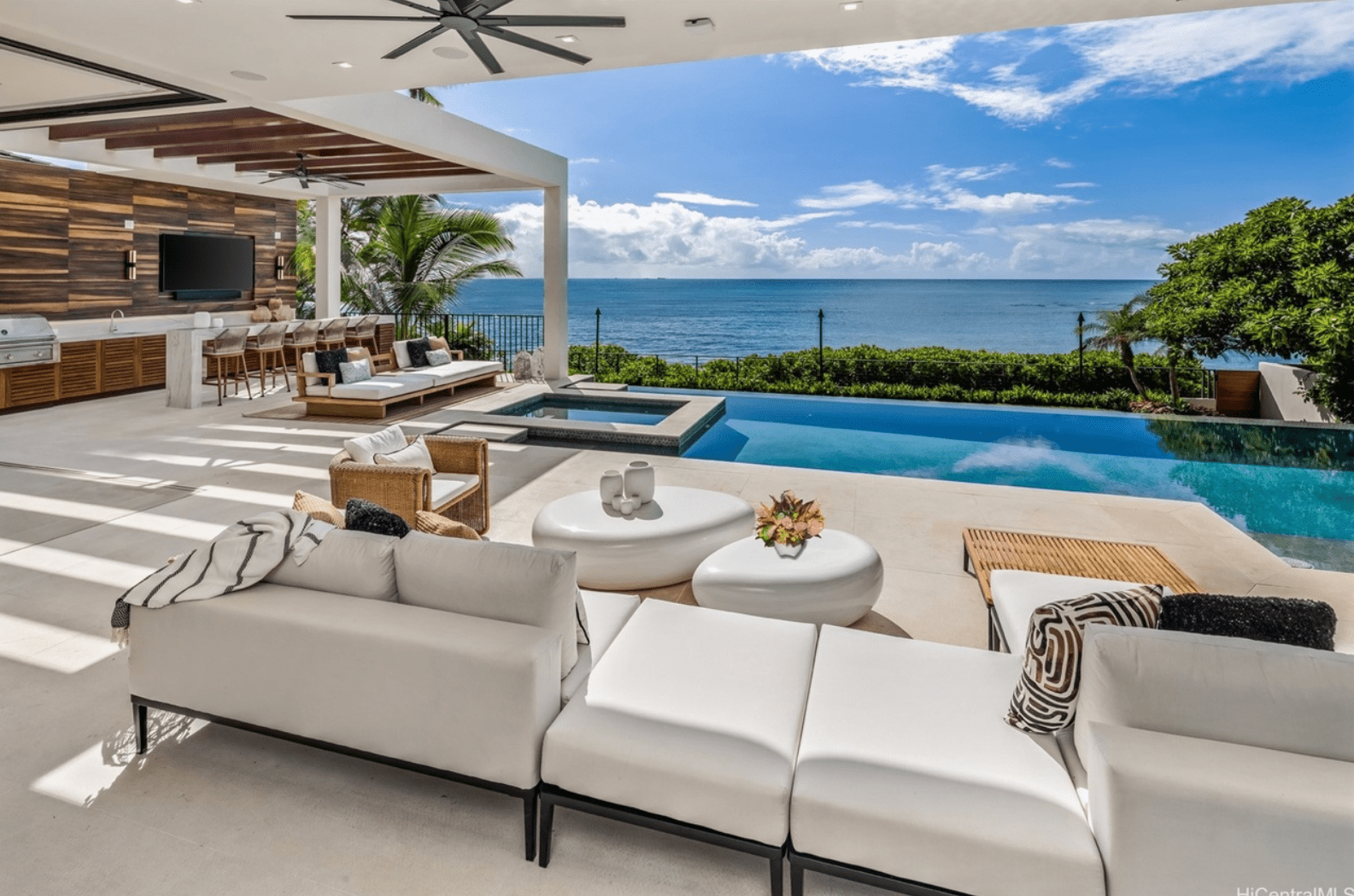

That’s how I found myself standing in a 6,700 square foot estate in Kahala with my wife, my dad, and our two kids. Five bedrooms, 5.5 baths, a free-form pool with a hot tub and cold plunge, a koi pond, and a gym with a climbing wall all on about at 15,000 sqft lot.

The house had been sitting on the market for over 200 days, which made it a perfect case study. Who buys these homes? And why was nobody buying this one?

The Family Verdict Took About Ten Minutes

My wife’s review: it feels too big. She’s right. We’re a family of four. Even living in it full-time, we’d realistically use a kitchen, a family room, four bedrooms, and the pool. The other 3,000 square feet would exist mainly to be cleaned, cooled, insured, and repaired.

My dad’s review was more sobering. The stairs were difficult for him. In one sentence, he eliminated an entire category of homes from our future search. If part of the reason we’re moving is to be there for my parents, what good is a nice house they can’t comfortably visit or live in? Any home we buy needs single-level living for them, and ideally an ohana unit in case a guest or a caregiver ever needs to stay long-term.

Then there’s the empty nest math nobody wants to do. Our youngest heads to college in 12 years. Soon after we’d move in in three years, it would be two adults rattling around 6,700 square feet like two marbles in a shoebox. That’s 3,350 square feet per person, plus an estimated $3,000 to $4,000 a month for the pool, tropical landscaping, and koi pond maintenance, before property taxes and insurance. Call it $150,000+ a year to maintain rooms we’d visit like museum exhibits.

So the house is a no for us at this price. But the tour raised a better question. If a family that could stretch for this home finds it impractical, who is actually buying at this price point?

I spent an hour talking with the listing agent to find out. Her answer was insightful.

“Most Buyers At This Price Point Are Buying Second Homes”

According to her, many buyers of $6-$10 million Honolulu homes don’t live in them full-time. Recent interest has come from Japanese nationals and West Coast buyers purchasing second homes they might use a month or two a year. Given the price points, I have to imagine many are entrepreneurs who had liquidity events, because even a $1 million a year W-2 job doesn’t comfortably support a $9 million vacation home.

Let that sink in. Someone pays $9 million for a house, plus $150,000 a year in carrying costs, to use it 30 days annually. Amortize the carrying costs alone and you’re at roughly $5,000 per night of actual use. Then there’s the $380,000 a year in risk-free income you could earn off $9 million. So we’re really talking more like $20,000 a night to live in the house for 30 days, or $10,000 a night if you visit for two months a year.

I guess that’s not terrible, especially if the housing market continues to go up. But that’s still quite a bit of money when you can stay at a resort for far less.

As someone who spent 13 years working in equities and 17 years writing about money, I couldn’t compute it. So I kept digging until I found the answer to these mega luxury purchases.

Here’s what I found. The rich don’t justify these purchases. They’ve simply graduated past the need to.

Justification #1: The Denominator Is Different

For our household, an $9 million house would consume too large a percentage of our net worth. My net worth rule for home buying says keep your primary residence at 30% of net worth or below, ideally closer to 20%. Violate it and the house starts owning you. So that would mean at least a $30 million net worth, and ideally, $45 million.

If you’re thinking of upgrading to a bigger, more expensive home, check out my income and net worth requirements to buy a home at all price points. It combines my 30/30/3 home buying rule with my net worth rule to show the minimum and ideal figures for homes priced from $200,000 all the way up to $50 million. Follow the guide and you’ll buy with confidence instead of buying with heartburn.

But the typical buyer of this home isn’t stretching. They’re likely worth $100 million to $300 million or more. At $150 million, an $9 million house is just 6% of net worth. That’s the equivalent of a household with a $1.5 million net worth buying an $90,000 condo. Nobody writes think pieces about whether that’s irresponsible.

The rule I recommend isn’t wrong. Their denominator is just so large for the rich the rule never gets tested. When your house could burn down uninsured and your lifestyle wouldn’t change, the question “can I afford this?” stops being a question.

The wealthier people get, the smaller the percentage of net worth they tend to spend on their primary residence. The ultra-rich have the lion’s share of their wealth in businesses and investments. The $9 million Kahala buyer isn’t breaking my rule. They’re following it to an extreme.

Justification #2: The House Is A Vault With A Pool

The ultra-wealthy don’t think of a vacation property estate as shelter. They think of it as a store of wealth.

Hawaii is not making more land next to the ocean. Supply is permanently constrained, global demand keeps rising, and trophy properties in world-class locations have historically held value like fine art, except you can swim in this art.

For international buyers, it’s also a currency and stability play. A hard asset in a politically stable jurisdiction, denominated in dollars, that your family can enjoy or escape to if things go sideways back home.

With the yen having weakened significantly against the dollar over the years, Japanese buyers who hold dollar assets or dollar-earning businesses are also playing a longer currency game than most of us bother to think about.

The month of annual use is incidental. The house is functionally a bond that happens to have a lanai. I’ve long argued real estate acts as a bond plus equivalent in a portfolio. The ultra-rich just take the concept to its logical extreme.

Justification #3: The Estate Planning Angle

When you die, assets included in your taxable estate receive a stepped-up cost basis to fair market value. Buy the Hawaii house for $9 million, hold it until it’s worth $20 million at death, and your kids inherit it with a $20 million basis. If they sell immediately, they owe essentially zero capital gains tax on $11 million of appreciation.

Now, before you conclude the rich pay no taxes, the estate tax still applies. In 2026, the federal exemption is $15 million per person, or $30 million per couple, with a 40% rate above that. A $150 million estate is still writing the IRS a check for roughly $48 million. Hawaii also levies its own estate tax of up to 20% on Hawaii real property, even for out-of-state owners, a detail I suspect half these buyers never priced in.

So the step-up isn’t a tax dodge. It’s basis arbitrage. Wealthy families deliberately keep low-basis assets like real estate inside the estate to capture the step-up, while gifting high-growth assets out early to dynasty trusts. The estate tax was going to hit their retained assets at 40% anyway. The step-up wipes out decades of capital gains as a consolation prize.

The house isn’t just a vault. It’s a pre-positioned inheritance, professionally gift-wrapped by an estate attorney everybody should talk to. Ironically, the poorer you are, the more important it may be to get your estate in order given probate court is far more expensive than distributing assets through a revocable living trust.

Justification #4: They’re Paying For Optionality, Not Occupancy

I’ve written for years that money’s greatest return is freedom. This is why the FIRE movement is so attractive to me. I’m happy to give up making more money to have more freedom. The ultra-rich apply this to real estate.

They aren’t buying 30 days of use. They’re buying the perpetual option to wake up tomorrow and decide to spend a month in Hawaii, with their own sheets, their own coffee maker, and nobody else’s hair in the shower drain. The empty 335 days don’t bother them because occupancy was never the point. The ability to occupy was.

Is that an insane price for optionality? By my math, yes. But I also pay for optionality constantly, just with more zeros removed. We have a paid off vacation property in Lake Tahoe worth about $750,000. The principle is identical. Only the scale offends.

Justification #5: They Don’t Do Cost-Per-Use Math Like The Rest Of Us

This was my final realization, and the most humbling one.

I calculated cost per night. I calculated price per occupied square foot post-empty-nest. Then I calculated carrying costs as a percentage of a safe withdrawal rate.

The ultra-rich do things differently. They vibe coded the numbers based on their feelings.

Cost-per-use math is a middle-class and mass-affluent survival skill. It’s how people like us built wealth in the first place. But past a certain net worth, the skill atrophies because it no longer serves a purpose.

When someone worth $200 million buys a $9 million house, asking them to justify it is like asking you to justify buying a $12 sandwich. Justify it to whom? It doesn’t matter.

That’s the real answer to my perplexity. I was asking a question the buyers stopped asking themselves a decade and eight figures ago.

The Takeaway

If you’ve ever felt behind because someone bought a house that seems impossibly expensive, understand you’re likely watching a different game with different rules. The buyer isn’t braver or smarter than you. They just have a denominator so large the decision required no courage at all.

Meanwhile, keep doing what actually works. Tour homes years before you plan to buy. Bring the people who will live in and visit the home, because your family will spot dealbreakers a listing photo never will. My wife needed one walkthrough to identify the maintenance trap. My dad needed one staircase to redefine our entire search criteria.

Keep running your cost-per-use math. Keep your primary residence at 30% of net worth or less. And before you upgrade to a bigger, more expensive home, run your numbers against my home buying guide below.

Being house rich and cash poor is no fun. You will likely be stressed out of your mind for the first year if you violate my guide above.

The discipline that seems unnecessary to the ultra-rich is exactly the discipline that might get you to their side of the table. And if you get there, I suspect you’ll keep doing the math anyway. Old habits built your wealth. No koi pond should retire them.

Readers, how do you explain paying $9 million for a home you use one month a year? Have you ever toured homes way above your price range to learn the market? And at what net worth, if any, would you stop doing cost-per-use math?

Invest In Real Estate Passively

To invest in real estate without the carrying costs, koi ponds, or climbing walls, check out Fundrise. Fundrise manages over $3 billion for investors, primarily in residential and industrial properties in the Sunbelt, where valuations are lower and yields are higher.

The ultra-rich buy $9 million Hawaii homes as stores of wealth because they can afford to lock up capital in a single illiquid asset. The rest of us can capture the same benefits, income, inflation protection, and diversification away from stocks, for as little as $10 and zero koi pond maintenance. I’ve personally invested over $500,000 with Fundrise to earn passive income and diversify my expensive San Francisco real estate holdings. Fundrise is a long-time sponsor of Financial Samurai.

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai began in 2009 and is one of the most trusted independently-run personal finance sites today. Everything is written based on firsthand experience because money is too important to be left up to pontification.

[ad_2]

Source link